All Categories

Featured

Table of Contents

Browsing Credit Obstacles in Dearborn Michigan

Economic shifts in 2026 have actually changed how households manage their month-to-month responsibilities. With interest rates holding at levels that challenge even disciplined savers, the conventional approaches of surviving are showing less effective. Many residents in Dearborn Michigan are looking at their financial declarations and seeing a larger part of their payments approaching interest rather than the principal balance. This shift has resulted in a renewed interest in structured debt management programs used by nonprofit firms.

The primary difficulty in 2026 remains the cost of unsecured credit. Credit card business have actually changed their danger designs, typically resulting in greater annual portion rates for consumers who carry balances from month to month. For those residing in your local area, these expenses can quickly surpass wage development, producing a cycle where the overall balance remains stagnant despite routine payments. Professionals concentrating on Debt Help suggest that intervention is most effective when started before missed out on payments start to damage credit history.

Comparing Combination Loans and Management Programs in 2026

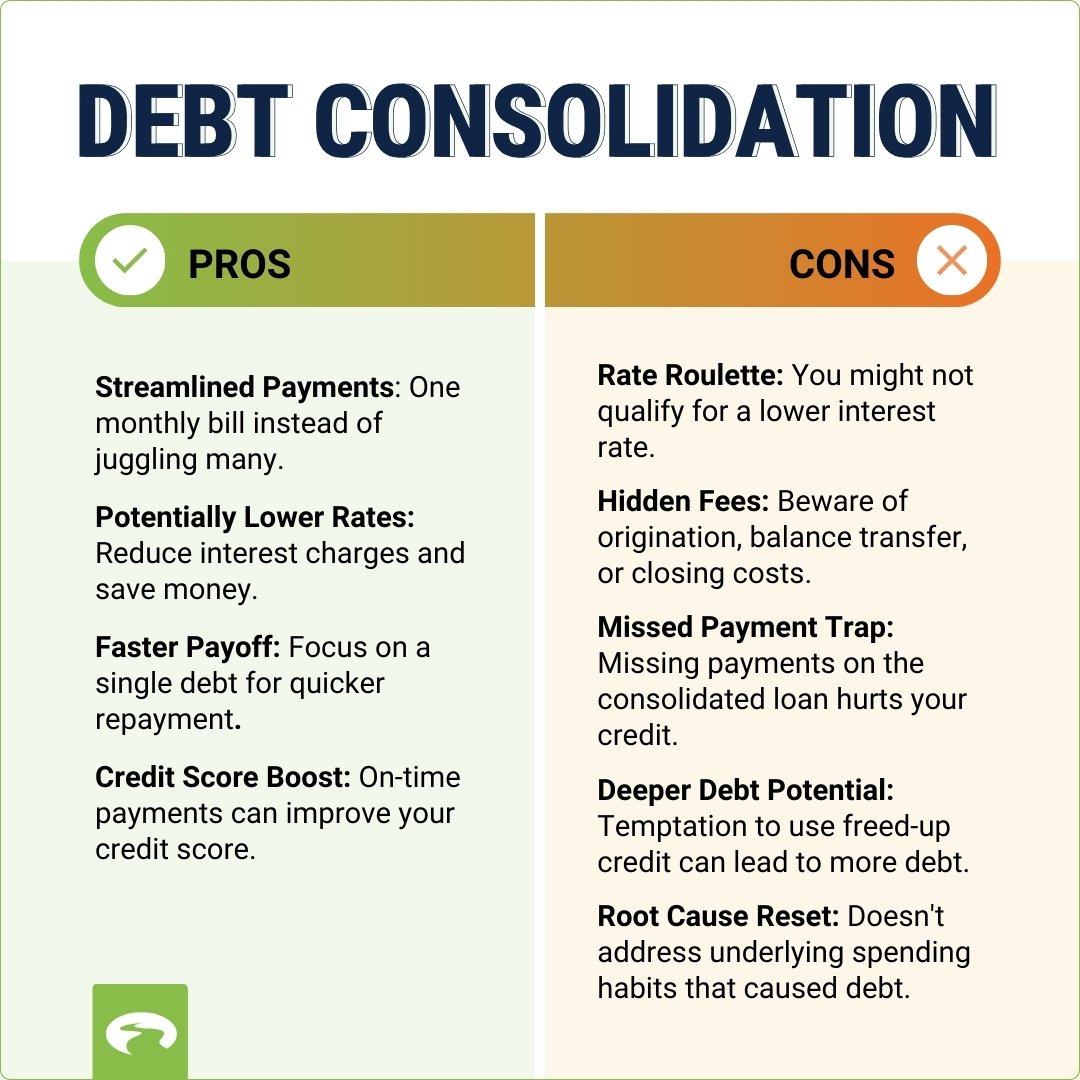

Financial strategies in 2026 often include selecting in between 2 unique paths: debt consolidation loans and debt management strategies. A combination loan includes taking out a brand-new, big loan to pay off several smaller sized financial obligations. This approach depends greatly on an individual's credit report and the accessibility of favorable terms from private loan providers. In the existing market, however, securing a low-interest individual loan has ended up being progressively challenging for those who are already carrying significant debt loads.

Reliable Debt Help Services provides a structured alternative to high-interest loans by working within the existing financial institution relationships. Unlike a loan, a debt management plan does not include borrowing more cash. Instead, it is a worked out arrangement helped with by a not-for-profit credit counseling company. These firms work with lenders to lower rates of interest and waive particular costs, enabling the customer to settle the full principal over a set duration, normally 3 to 5 years. For numerous in the surrounding area, this method provides a clear timeline for reaching zero balance without the need for a brand-new credit line.

The difference is substantial for long-term monetary health. While a loan just moves debt from one place to another, a management plan focuses on methodical payment and behavioral change. Therapy sessions related to these programs frequently include budget plan evaluations that help participants determine where their money goes each month. This educational component is a trademark of the 501(c)(3) nonprofit model, which prioritizes customer stability over revenue margins.

The Mechanics of Rates Of Interest Settlement in your local area

One of the most effective tools offered to consumers in 2026 is the capability of credit therapy companies to work out straight with major banks and card providers. These settlements are not about choosing less than what is owed-- a process that typically damages credit-- but about making the repayment terms manageable. By decreasing a 24 percent rate of interest to 8 or 10 percent, a program can shave years off the repayment duration and save the consumer countless dollars.

Individuals frequently look for Credit Relief in Michigan when handling several lender accounts becomes a logistical problem. A management strategy simplifies this by consolidating multiple month-to-month bills into a single payment. The not-for-profit company then distributes that payment to the various lenders according to the negotiated terms. This structure decreases the probability of late charges and guarantees that every account remains in great standing. In Dearborn Michigan, this simplification is frequently the primary step toward restoring control over a family budget plan.

Lenders are typically willing to take part in these programs due to the fact that they prefer getting routine, complete payments over the threat of an account going into default or insolvency. By 2026, numerous monetary organizations have structured their cooperation with Department of Justice-approved agencies to help with these plans more effectively. This cooperation benefits the consumer through reduced tension and a predictable path forward.

Strategic Debt Repayment in across the country

Housing and credit are deeply connected in 2026. Numerous households in various regions discover that their ability to certify for a mortgage or preserve their current home depends upon their debt-to-income ratio. High credit card balances can inflate this ratio, making it challenging to gain access to beneficial housing terms. Nonprofit agencies that provide HUD-approved real estate therapy frequently incorporate debt management as part of a bigger method to stabilize a household's living circumstance.

The impact on credit report is another element to consider. While a debt management strategy needs closing the accounts included in the program, the consistent on-time payments typically assist reconstruct a credit profile with time. Unlike financial obligation settlement, which involves stopping payments and letting accounts go to collections, a management plan reveals a dedication to honoring the initial financial obligation. In the eyes of future loan providers, this difference is crucial.

- Lowered interest rates on credit card accounts.

- Waived late fees and over-limit charges.

- Single month-to-month payment for numerous unsecured debts.

- Expert guidance from qualified credit therapists.

- Education on budgeting and monetary literacy.

As 2026 progresses, the function of monetary literacy has actually moved from a luxury to a need. Understanding the difference between secured and unsecured financial obligation, the effect of intensifying interest, and the legal protections available to customers is essential. Not-for-profit agencies act as a resource for this details, providing services that surpass simple financial obligation repayment. They provide the tools required to avoid future cycles of debt by mentor individuals how to construct emergency situation funds and handle capital without counting on high-interest credit.

Long-Term Stability Through Structured Planning

The decision to get in a financial obligation management program is often a turning point for households in Dearborn Michigan. It marks a shift from reactive costs to proactive planning. While the program needs discipline-- specifically the commitment to stop utilizing charge card while the strategy is active-- the outcome is a debt-free status that supplies a foundation for future conserving and investment.

Financial consultants in 2026 highlight that there is no one-size-fits-all option, but for those with substantial unsecured debt and a consistent income, the structured approach of a nonprofit plan is frequently the most sustainable choice. It prevents the high fees of for-profit settlement companies and the long-term credit damage of bankruptcy. Instead, it offers a middle course that stabilizes the needs of the consumer with the requirements of the lender.

Success in these programs depends upon transparency and consistent communication with the therapist. By examining the spending plan quarterly and making modifications as living costs alter in your region, individuals can remain on track even when unanticipated costs arise. The goal is not simply to pay off what is owed, however to leave the program with a different viewpoint on how to utilize credit in such a way that supports, instead of hinders, monetary progress.

Eventually, the role of debt management in a 2026 monetary technique is to offer a clear exit from high-interest commitments. By focusing on primary decrease and interest settlement, these strategies permit homeowners in Dearborn Michigan to reclaim their earnings and concentrate on their long-term goals. Whether the goal is buying a home, saving for retirement, or simply minimizing day-to-day stress, a structured repayment plan offers the framework essential to achieve those ends.

{kind=link}

Latest Posts

Learning Financial Literacy in Newark New Jersey

Why 2026 Is the Time to Simplify Your Debt

Is Your Regional Bank Using AI Relatively?